Frequently Asked Questions

Section 1: Settlement Frequently Asked Questions

Section 2: Steinhoff Allocation Plan Frequently Asked Questions

Settlement Frequently Asked Questions

Steinhoff International Holdings N.V. (“SIHNV”) and Steinhoff International Holdings Proprietary Limited (“SIHPL”) (together with their subsidiaries, the “Steinhoff Group”)

These Settlement Frequently Asked Questions have been published to assist claimants with SIHNV’s and SIHPL’s global settlement of claims (the “Steinhoff Group Settlement”) and are only non-binding guidance for claimants and should be read in conjunction with the Dutch SoP Scheme and S155 Scheme, as applicable. If there is an inconsistency between these Settlement Frequently Asked Questions and the Dutch SoP Scheme and/or S155 Scheme, the provisions of the Dutch SoP Scheme and S155 Scheme will prevail.

Please note that the answers do not constitute legal advice. Please consider the terms of the Dutch SoP Scheme and S155 Scheme carefully to make sure you understand your position. The Dutch SoP Scheme and S155 Scheme are complex documents and claimants should obtain independent legal, financial and tax advice in relation to the Schemes and the claim administration. Only the Schemes (including the Schedules and Annexes thereto) contain the terms and conditions on the basis of which any claimant may or may not hold any entitlement to any distribution. These Frequently Asked Questions are not intended to reflect all of such terms and conditions and do not in any way alter, modify, supplement or otherwise grant such right or obligation to any claimant, any member of the Steinhoff Group or the SRF (as defined below). This is a document that in itself does not have any legal power or authority. None of the Steinhoff entities nor their advisers are providing any advice to claimants or any other party.

Further information on the Schemes and the settlement (including detailed Frequently Asked Questions on the Allocation Plan) is available on the following website: www.steinhoffsettlement.com

Part 1 – The Steinhoff Group Settlement

1. What is the Steinhoff Group Settlement?

- SIHNV and SIHPL have formulated a global settlement of the claims against them with settlement amounts for various claimant groups in light of:

- the characteristics of, and risks associated with, their claims;

- the Steinhoff Group’s ability to continue trading and to maximise the asset values available to it; and

- the likely outcomes for participating claimants if the Steinhoff Group was unable to settle the claims and liquidation ensued.

- The Steinhoff Group Settlement is made on the basis that it does not represent an admission of any liability in respect of any of the various claims made against any member of the Steinhoff Group or any directors, officers, employees or advisors, past or present.

- Separately, and as announced by the Steinhoff Group on 15 February 2021 and 23 March 2021, eligible claimants may also receive a payment from additional funds made available by Deloitte and the D&O Insurers. To receive such payment, eligible claimants must agree to the terms of the offers from Deloitte and the D&O Insurers by selecting the appropriate option on the claim form. For more information: www.steinhoffsettlement.com/settlements-deloitte-and-do.aspx.

- For the purposes of these Settlement Frequently Asked Questions, “Steinhoff Shares” comprise:

- common stock shares in SIHNV with ISIN NL0011375019; and

- common stock shares in SIHPL with ISIN ZAE000016176.

- SIHNV has concluded a Dutch “suspension of payments” procedure (“Dutch SoP”) and, in parallel, SIHPL has concluded a statutory compromise process under South African law (“South African S155”). The Dutch SoP related only to SIHNV and the South African S155 related only to SIHPL. These processes did not directly affect any of the other entities in the Steinhoff Group nor any of its operating businesses.

- SIHNV’s composition plan as submitted in the Dutch SoP (“Dutch SoP Scheme”) and SIHPL’s plan under the South African S155 (“S155 Scheme”) (together the “Schemes”) are available at www.steinhoffsettlement.com/case-documents.aspx.

2. What happens next and how does the settlement process work?

- Steinhoff Recovery Foundation (the “SRF”) has been established to (in short) administer and oversee the distribution of the settlement payments pursuant to the Schemes. The SRF is a Dutch foundation (stichting) established as an independent entity governed by a board of newly appointed directors with majority independence from the Steinhoff Group (see for more information about the SRF the Steinhoff Allocation Plan Frequently Asked Questions – Part B).

- The SRF has engaged Computershare as claims administrator (the “Claims Administrator”) to assist with the implementation of the Steinhoff Group Settlement, including the administration of claims and the distribution process.

- Shareholders who held Steinhoff Shares at close of business on 5 December 2017 and any other potential claimants are advised to seek independent legal, financial and tax advice in respect of the Steinhoff Group Settlement and the Schemes.

3. What should I do to take part in the global settlement?

- Claimants who wish to claim a distribution should file their claims prior to the Bar Date (23:59:59 SAST on 15 May 2022) by completing the relevant claim form on www.steinhoffsettlement.com

- As a condition to receiving payment in accordance with the Schemes (if any), the relevant filed claim form must be complete and valid. Further details in this regard are contained in the relevant Claim Form and in the Schemes and the schedules thereto (especially Schedule 2 to the SRF and Claims Administration Conditions (Required Claim Information). These SRF and Claims Administration Conditions are attached as Schedule 2 to the SoP Scheme and are available on www.steinhoffsettlement.com).

- See also Steinhoff Allocation Plan Frequently Asked Questions (especially part C).

4. What are the different groups of claimants?

- There are two groups of (litigation) claimants that fall under the Steinhoff Group Settlement: contractual claimants and “Market Purchase Claimants” (“MPCs”). The third group of claimants comprise the financial creditors.

- Contractual claimants are claimants who hold claims against Steinhoff which:

- relate to the alleged accounting irregularities; and

- arise as a result of a contractual arrangement entered into with SIHPL between 1 March 2009 and 7 December 2015 or SIHNV between 7 December 2015 and 5 December 2017, whereby SIHPL or SIHNV shares were purchased or SIHPL or SIHNV shares were issued or exchanged as consideration for the contribution of that contractual claimant's business or assets.

- MPCs are claimants who have an “MPC Relevant Claim”. An MPC Relevant Claim is (in short) a claim against SIHPL and/or SIHNV relating to alleged accounting irregularities and arising as a result of purchasing, acquiring or having a transfer in (as defined in the Steinhoff Allocation Plan – Schedule 3 to the SoP Scheme) of:

- either SIHPL shares listed on the Johannesburg Stock Exchange (“JSE”) between open of business on 2 March 2009 and close of business on 6 December 2015 (which were subsequently converted to SIHNV Shares), or SIHNV shares listed on the JSE or the Frankfurt Stock Exchange (“FSE”) between close of business on 6 December 2015 and close of business on 5 December 2017, and in each case continued to hold at least some of those shares (or, in the case of SIHPL shares, SIHNV shares received in exchange for them) at close of business on 5 December 2017; and/or

- SIHPL Shares listed on the JSE prior to open of business on 2 March 2009 and holding such shares at close of business on 5 December 2017 on the basis of the LIFO matching process described in the Steinhoff Allocation Plan (Schedule 3 to the SoP Scheme).

- The financial creditors are those who have claims arising against Steinhoff under, out of or in connection with contingent payment undertakings (being debt instruments).

5. How and why has the settlement changed since it was originally announced in 2020?

Developments leading to the July 2021 update:

- Since the announcement of the Steinhoff Group Settlement in July 2020, the Steinhoff Group’s underlying businesses have shown resilient financial and operational performance and an increase in the value of a number of its investments.

- The global settlement was constructed to present claimants with a better outcome than the likely alternative (i.e. liquidation).

- In line with that approach, and given the increase in value of underlying investments, positive currency movements and improved outlook, SIHNV and SIHPL announced on 16 July 2021 that they would increase the total settlement offer under the Steinhoff Group Settlement.

Developments leading to the August 2021 update:

- Whilst the revised July 2021 settlement offer received positive responses, SIHPL and SIHNV concluded that there was insufficient support to achieve certainty of a positive outcome in a vote on the S155 Scheme.

- Additionally, there remained material uncertainty posed by the various legal disputes against SIHPL arising from legacy accounting issues and, more recently, the settlement arrangements at the SIHPL level.

- Recognising that the focus of disputes shifted to primarily concern the settlement arrangements at the SIHPL level, and considering the levels of support needed to obtain a positive outcome in a vote on the S155 Scheme, Steinhoff announced via the a further and final contribution by SIHPL to the settlement consideration in August 2021.

- The August 2021 proposal included an additional and separate amount made available by SIHPL for SIHPL market purchase claims only, which will be allocated proportionately among SIHPL MPCs based on their respective claims (as determined under the existing rules in the Dutch SoP Scheme) on a pro rata basis.

- The S155 Scheme and the Dutch SoP Scheme were amended to reflect the terms of the updates in July 2021 and the August 2021.

6. Why didn’t the board simply liquidate SIHNV and/or SIHPL?

- Liquidations would not add value. Rather, a liquidation of SIHNV and/or SIHPL, and resulting accelerated sales or liquidation processes in respect of their direct and indirect interests in companies in the Steinhoff Group and substantial costs of liquidation would, in SIHNV’s and SIHPL’s view, materially impair the value of assets available for distribution to their respective stakeholders (including claimants) and would adversely affect the timing and diminish the amount of the claimants’ recoveries in comparison to the Steinhoff Group Settlement.

- Such processes could also be expected to adversely affect the interests of the Steinhoff Group’s broader stakeholders, including customers and employees.

7. Can any further proceedings be brought against Steinhoff in respect of the SIHNV and SIHPL shares?

- No, the Schemes have resulted in the full and final release of all claims (other than those referred to below) against companies in the Steinhoff Group arising as a result of the alleged accounting irregularities. Due to the nature of the Schemes and court proceedings used to give effect to the settlement, this includes the claims of those claimants who did not participate in the settlement.

- However, not all claims against SIHNV or SIHPL will be compromised under the Schemes. Certain disputed claims against SIHNV will continue to be defended on the basis that any finally adjudicated claim or agreed settlement amount will be subject to the same SIHNV recovery rate payable to MPCs and contractual claimants of SIHNV. Similarly, one disputed contractual claim against SIHPL will continue to be defended on the basis that any finally adjudicated claim or agreed settlement amount will be subject to the same recovery rate payable to contractual claimants of SIHPL.

8. What are the benefits of the Steinhoff Group Settlement?

The boards of SIHNV and SIHPL believe that the Steinhoff Group Settlement is in the best interests of SIHNV and SIHPL, respectively. In particular, the Steinhoff Group Settlement will:

- provide participating claimants with certainty of outcome and recovery relative to the cost and uncertainty associated with protracted, expensive and unpredictable court processes in pursuing their claims;

- provide consistent treatment of recovery to similar claimants to the extent possible;

- offer a more favourable and more certain recovery on their claims as compared to a liquidation of SIHNV or SIHPL;

- resolve a very substantial proportion of the material contingent liabilities faced by SIHNV and SIHPL as a result of the ongoing litigation;

- include a debt term extension from the Steinhoff Group’s financial creditors under the SIHNV and SIHPL CPUs which will be matched by the intra-group creditors;

- not affect the rights of current trade creditors;

- assist the continuing efforts to support the operating businesses in the Steinhoff Group to preserve and realise business value for the Steinhoff Group’s stakeholders and employees;

- reduce the current burden on the Steinhoff Group of the very material costs spent litigating numerous legal proceedings across multiple jurisdictions; and

- reduce the proportion of Steinhoff Group management time committed to the supervision and conduct of the various legal proceedings, allowing management to concentrate on the continued improvement of the underlying businesses and development of plans to realise value and de-leverage the Steinhoff Group’s balance sheet.

9. How are the Deloitte Firms supporting the Steinhoff Group Settlement?

- SIHNV and SIHPL have reached an agreement with Deloitte Accountants B.V. and Deloitte & Touche South Africa (together, the “Deloitte Firms”), pursuant to which the Deloitte Firms have made additional compensation available to certain Steinhoff claimants:

- (i) an amount of up to EUR 55.34 million for distribution to the MPCs (the “Deloitte Settlement Fund”); and

- (ii) an amount of EUR 15 million for distribution to certain contractual claimants.

- MPCs or their representatives who in due course wish to receive a part of the Deloitte Settlement Fund must use the same Claim Form as the Claim Form to be used for submitting their claims to the Steinhoff Group Settlement. The Claim Forms and further relevant information are available on www.steinhoffsettlement.com.

- It is important to note that the Deloitte Firms do not in any way admit liability for the losses incurred by Steinhoff and its stakeholders as a result of the accounting irregularities at Steinhoff.

10. How are the D&O Insurers and the D&Os supporting the Steinhoff Group Settlement?

- SIHNV and SIHPL have also reached an agreement with certain insurance companies underwriting Steinhoff’s (primary and excess) Directors and Officers insurance policy (the “D&O Insurers”) and certain directors and officers who work or have worked for or been associated with a Steinhoff Group company (the “Settling D&Os”), pursuant to which D&O Insurers will make additional compensation available to certain Steinhoff claimants:

- (i) an amount of up to EUR 55.5 million for distribution to the MPCs (the “D&O Insurers Settlement Fund”); and

- (ii) an amount of EUR 15 million for distribution to certain contractual claimants.

- MPCs or their representatives who in due course wish to apply to receive a part of the D&O Insurers Settlement Fund must use the same Claim Form as the Claim Form to be used for submitting their claims to the Steinhoff Group settlement. The Claim Forms and further relevant information are available on www.steinhoffsettlement.com.

- It is important to note that D&O Insurers and the Settling D&Os do not in any way admit liability for the losses incurred by Steinhoff and its stakeholders as a result of the accounting irregularities at Steinhoff.

11. How and why has the proposed global settlement changed since 2020?

- As mentioned in part 1, question 1 above, the proposed global settlement was first announced via the July 2020 Offer and amended in the October 2020 Settlement Term Sheet.

- Developments leading to the July 2021 Settlement Term Sheet:

- Since the announcement of the settlement proposal via the July 2020 Offer, the Steinhoff Group’s underlying businesses have shown resilient financial and operational performance and an increase in the value of a number of its investments.

- The global settlement proposal was constructed to present claimants with a better outcome than the likely alternative (i.e. liquidation).

- In line with that approach, and given the increase in value of underlying investments, positive currency movements and improved outlook, SIHNV and SIHPL announced on 16 July 2021 that they would increase the total settlement offer under the Steinhoff Group global settlement in the form of the July 2021 Settlement Term Sheet.

- Developments leading to the August 2021 Proposal

- Whilst the revised settlement offer set out in the July 2021 Settlement Term Sheet received positive responses, SIHPL and SIHNV concluded that there was insufficient support to achieve certainty of a positive outcome in a vote on the S155 Scheme Proposal.

- Additionally, there remained material uncertainty posed by the various legal disputes against SIHPL arising from legacy accounting issues and, more recently, the proposed settlement arrangements at the SIHPL level. For further detail on the recent disputes against SIHPL see the recent press releases, in particular the 16 July 2021 press release, published at https://www.steinhoffinternational.com/sens.php.

- Steinhoff continues to believe that a global settlement is the preferable approach to resolve all or substantially all of the current disputes and claims. Therefore, recognising that the focus of the more recent disputes concern the proposed settlement arrangements at the SIHPL level, and considering the levels of support needed to obtain a positive outcome in a vote on the S155 Scheme Proposal, Steinhoff announced via the August 2021 Proposal a further and final contribution by SIHPL to the settlement consideration.

- The August 2021 Proposal includes an additional and separate amount made available by SIHPL for SIHPL market purchase claims only, which will be allocated proportionately among SIHPL MPCs based on their respective claims (as determined under the existing rules in the Dutch SoP Scheme Proposal) on a pro rata basis.

- The S155 Scheme Proposal and the Dutch SoP Scheme Proposal have been amended to reflect the terms of the July 2021 Offer and the August 2021 Proposal, and revised versions are available at https://www.steinhoffinternational.com/settlement-litigation-claims.php.

12. What indications of support for the proposed global settlement have you had?

- Steinhoff believes the terms of the proposed settlement are fair and realistic in the circumstances and urges claimants to take this opportunity to agree a settlement.

- Vereniging van Effectenbezitters (“VEB”) has issued a support statement and withdrawn its collective (class) action in the Netherlands and recommended the proposal.

- Steinhoff has also received letters of support for the proposed settlement from various representatives of MPCs as well as contractual claimants. Reference is made to, among others, the press release dated 31 March 2021 (www.steinhoffsettlement.com/updates-and-press-releases.aspx).

- Steinhoff has received confirmation that the active claimant group, Hamilton, supports in principle the Steinhoff global settlement based on the August 2021 Proposal, and will withdraw from the class composition application which has been adjourned until 13 August 2021 on that basis. Hamilton’s final approval of the S155 proposal will be subject to the ongoing claim verification process.

- SIHPL has also received confirmation that key financial creditors - funds managed or advised by The Baupost Group, LLC, Farallon Capital, Sculptor Capital Management and Silver Point Capital - are supportive of the further revisions to the settlement terms as set out in the August 2021 Proposal.

13. What approvals do you require?

- In order for the proposed global settlement to proceed, approval is required from sufficient claimants to approve the Schemes.

- A consent request was launched on 9 October 2020 to obtain the formal support of the financial creditors for the terms and proposed implementation of the settlement (the “October 2020 Consent Request”). The October 2020 Consent Request was approved by the financial creditors in respect of all relevant financial instruments, with the exception of the Company’s “SEAG Contingent Payment Undertaking”. SIHNV then undertook an English law scheme of arrangement to obtain the requisite approval under the SEAG Contingent Payment Undertaking. The terms of this scheme applicable at that time were subsequently approved and on 5 February 2021 sanctioned by the High Court of England.

- A further financial creditor approval is required for the updated terms of the S155 Scheme pursuant to the July 2021 Settlement Term Sheet and the August 2021 Proposal. The necessary consent request has been prepared and will be launched shortly following the updated Schemes (reflecting the revised proposal) being made available. Responses to this further consent request are expected prior to the S155 Scheme creditors’ meetings, which are currently anticipated to occur by mid-September 2021.

- SIHNV applied to Finsurv for consent to the cross-border payments to be made as part of the proposed settlement and received such approval on 25 November 2020. The approval is valid for 12 months. Further approvals will be sought to the extent required in respect of the terms to be submitted under the Schemes. In particular, the Steinhoff Group is in the process of applying for Finsurv consent with respect to the recent revisions to the S155 Scheme Proposal incorporating the terms announced in the July 2021 Settlement Term Sheet and August 2021 Proposal.

14. Why didn’t the Board simply liquidate SIHNV and/or SIHPL?

- A liquidation would not add value. Rather, a liquidation of SIHNV and/or SIHPL, and resulting accelerated sales or liquidation processes in respect of their direct and indirect interests in companies in the Steinhoff Group and substantial costs of liquidation would, in SIHNV’s and SIHPL’s view, materially impair the value of assets available for distribution to their respective stakeholders (including litigants) and would adversely affect the timing and diminish the amount of the claimants’ recoveries in comparison to the proposed settlement.

- Such processes could also be expected to adversely affect the interests of the Steinhoff Group’s broader stakeholders, including customers and employees.

15. If the proposed settlement is successful, could any further proceedings be brought against Steinhoff in respect of the SIHNV and SIHPL shares?

- No. If the proposed settlement is successful it will lead to the full and final release of all claims (other than those referred to below) against companies in the Steinhoff Group arising as a result of the alleged accounting irregularities. Due to the nature of the court proceedings being used to give effect to the proposed settlement, this will include the claims of those claimants who did not participate in the proposed settlement.

- However, not all claims against SIHNV or SIHPL will be compromised under the Schemes. Certain disputed claims against SIHNV will continue to be defended on the basis that any finally adjudicated claim or agreed settlement amount will be subject to the same SIHNV recovery rate payable to MPC and contractual claimants of SIHNV. Similarly, one disputed contractual claim against SIHPL will continue to be defended on the basis that any finally adjudicated claim or agreed settlement amount will be subject to the same recovery rate payable to contractual claimants of SIHPL. Certain other claims against SIHPL that do not qualify as either MPCs or contractual claims will not be subject to the S155 Scheme Proposal at all. SIHPL will continue to dispute such claims, which will be payable in full to the extent that they are ultimately upheld by way of final adjudication or agreed settlement.

16. What are the likely benefits of the proposed settlement?

The boards of SIHNV and SIHPL believe that the proposed global settlement and the proposed implementation processes, through the Schemes, are in the best interests of SIHNV and SIHPL, respectively. In particular, the proposed settlement will:

- provide participating claimants with certainty of outcome and recovery relative to the cost and uncertainty associated with protracted, expensive and unpredictable court processes in pursuing their claims;

- provide consistent treatment of recovery to similar claimants to the extent possible;

- offer a more favourable and more certain recovery on their claims as compared to a liquidation of SIHNV or SIHPL;

- resolve a very substantial proportion of the material contingent liabilities faced by the Company and SIHPL as a result of the ongoing litigation;

- include a debt repayment term extension from the Steinhoff Group’s financial creditors under the SIHNV and SIHPL CPUs which will be matched by the intra-group creditors;

- not affect the rights of current trade creditors;

- assist the continuing efforts to support the operating businesses in the Steinhoff Group to preserve and realise business value for the Steinhoff Group’s stakeholders and employees;

- reduce the current burden on the Steinhoff Group of the very material costs spent litigating numerous legal proceedings across multiple jurisdictions; and

- reduce the proportion of Steinhoff Group management time committed to the supervision and conduct of the various legal proceedings, allowing management to concentrate on the continued improvement of the underlying businesses and development of plans to realise value and de-leverage the Steinhoff Group’s balance sheet.

17. How are Deloitte supporting the Steinhoff Group Settlement?

SIHNV and SIHPL have reached an agreement with the Deloitte Firms pursuant to which the Deloitte Firms will, subject to the fulfilment of certain conditions, support the proposed Steinhoff global settlement proposal.

This means that provided that Steinhoff successfully completes the contemplated Dutch SoP and the S155 Scheme and certain other conditions are fulfilled, the Deloitte Firms will, in exchange for certain waivers and releases make additional compensation available to certain Steinhoff claimants, including the MPC Claimants:

- an amount of up to EUR 55.34 million for distribution to the MPC Claimants (the “Deloitte Settlement Fund”); and

- an amount of EUR 15 million for distribution to certain contractual claimants.

MPC Claimants or their representatives who in due course wish to apply to receive a part of the Deloitte Settlement Fund must use the same Claim Form as the Claim Form to be used for submitting their claims in the Dutch SoP and the S155 Scheme. The Claim Forms and further relevant information are available on www.steinhoffsettlement.com.

Eligible contractual claimants will receive individual notice from Steinhoff on the manner in which they can apply to receive a share of the amount offered to them

It is important to note that the Deloitte Firms do not in any way admit liability for the losses incurred by Steinhoff and its stakeholders as a result of the accounting irregularities at Steinhoff.

18. How are the D&O Insurers and the D&Os supporting the Steinhoff Group Settlement?

SIHNV and SIHPL have reached an agreement with certain insurance companies underwriting Steinhoff’s (primary and excess) Directors and Officers insurance policy (the “D&O Insurers”) and certain directors and officers who work or have worked for or been associated with a Steinhoff Group company (the “Settling D&Os”), pursuant to which D&O Insurers and Settling D&Os will, subject to the fulfilment of certain conditions, support the proposed Steinhoff global settlement proposal.

This means that provided that Steinhoff successfully completes the contemplated Dutch SoP and the S155 Scheme and certain other conditions are fulfilled, D&O Insurers (on behalf of the Settling D&Os) will, in exchange for certain waivers and releases including for all former directors and officers and other employees who work, or have in any way worked, for or been associated with a current or former Steinhoff group company, make additional compensation available to certain Steinhoff claimants, including the MPC Claimants:

- an amount of up to EUR 55.5 million for distribution to the MPC Claimants (the “D&O Insurers Settlement Fund”); and

- an amount of EUR 15 million for distribution to certain contractual claimants.

MPC Claimants or their representatives who in due course wish to apply to receive a part of the D&O Insurers Settlement Fund must use the same Claim Form as the Claim Form to be used for submitting their claims in the Dutch SoP and the S155 Scheme. The Claim Forms and further relevant information are available on www.steinhoffsettlement.com.

Eligible contractual claimants will receive individual notice from Steinhoff on the manner in which they can apply to receive a share of the amount offered to them.

It is important to note that D&O Insurers and the Settling D&Os do not in any way admit liability for the losses incurred by Steinhoff and its stakeholders as a result of the accounting irregularities at Steinhoff.

Part 2 – The Implementation Proceedings

1. What are the Dutch SoP and S155 Scheme and who do they apply to?

- The Steinhoff Group settlement has been given effect using two inter-conditional court proceedings: (i) proceedings under section 155 of the South African Companies Act 71 of 2008, which has been used to give effect to the settlement of claims against SIHPL; and (ii) Dutch suspension of payment proceedings, which has been used to give effect to the settlement of claims against SIHNV.

- The Dutch SoP relates only to SIHNV and the S155 Scheme relates only to SIHPL. These processes do not directly affect any of the other entities in the Steinhoff Group nor any of its operating businesses.

2. What is the Dutch SoP Scheme and who does it apply to?

- The Dutch SoP Scheme is the document which sets out the terms of the Steinhoff Group Settlement which was approved by the court in the Dutch SoP.

- The Dutch SoP Scheme applies to claimants who have a claim against SIHNV (i.e. including a claim arising because they purchased SIHNV Shares in the period from 7 December 2015 to 5 December 2017, and continued to hold these until close of business on 5 December 2017).

- The Dutch SoP Scheme is accessible on www.steinhoffsettlement.com.

3. What is the S155 Scheme Proposal and who does it apply to?

- The S155 Scheme is the document which sets out the terms of the Steinhoff Group Settlement which was approved by the court in the S155 Scheme.

- The S155 Scheme applies to claimants who have a claim against SIHPL (i.e. because they purchased or otherwise acquired SIHPL Shares in the period prior to 6 December 2015 and continued to hold these until close of business on 5 December 2017 or because they have contractual claims against SIHPL or because they are financial creditors of SIHPL in respect of claims against SIHPL arising under, out of or in connection with contingent payment undertakings). Such claimants may be eligible to cast their vote on whether the Steinhoff Group Settlement should be approved in the South African S155 Scheme.

- The S155 Scheme is available at www.steinhoffsettlement.com.

4. I purchased Steinhoff shares, how do the Schemes apply to me??

- Both the S155 Scheme and the Dutch SoP have been approved by the relevant courts. The Schemes were the processes by which the Steinhoff Group Settlement was implemented and contain the rules by which to eligible claimants will receive compensation (if any). The Allocation Plan and Allocation Plan Frequently Asked Questions include details on how claims are allocated compensation.

- When you submit your claim to the Claims Administrator (through the online claim portal or a claim form provided by the Claims Administrator), you submit your claims against SIHNV and/or SIHPL, as the case may be.

5. I have received an Initial SIHPL Claim Valuation Notification from Computershare. What does this mean?

- The Initial SIHPL Claim Valuation Notification relates solely to the S155 Scheme and is intended to notify you of: (i) the fact that Computershare, as the Claims Administrator, has initially determined that the claim you filed for the purposes of the S155 Scheme constitutes an “MPC Relevant Claim” pursuant to the S155 Scheme and can be accepted; and (ii) the claim value of that claim insofar as it relates to SIHPL Shares (the “Initial SIHPL Claim Value”).

- For the avoidance of doubt, the Initial SIHPL Claim Value ascribed to your claim has been initially calculated solely in relation to the SIHPL Shares filed in the claim and is not conclusive for the purposes of distribution. No rights can be derived from the Initial SIHPL Claim Value Notification in the context of the distribution. Prior to a distribution being made, the Claims Administrator may re-verify the claim. In respect of that process, you will be entitled to cure any deficiencies and may avail yourself of the full Dispute Committee process for distribution purposes as set out in the S155 Scheme.

6. I have already received a Deficiency Notification from Computershare. What does this mean?

- If you received a Deficiency Notification prior to the S155 Scheme meeting (which occurred on 6 September 2021), it is likely it related solely to the S155 Scheme and was intended to notify you of your ineligibility to participate in and vote at the S155 Scheme meeting, on the basis that one or more deficiencies have been found in respect of the claim submitted by you in the context of the S155 Scheme (i.e. only in respect of your SIHPL Shares).

- If you have received a Deficiency Notification since the S155 Scheme meeting, then your claim is considered to have a deficiency which may limit (in whole or in part) any distributions if not cured.

- Please note that the Deficiency Notification does not necessary mean that you are not eligible to receive a distribution . For distribution purposes, you will be entitled to cure any deficiencies and may avail yourself of the full Dispute Committee process as set out in the S155 Scheme. If you are able to cure these deficiencies (and any potential further deficiencies that are notified to you by the Claims Administrator at a later stage), you may still be eligible to receive a distribution from the settlement fund. The Claims Administrator will contact you in due course with an outline of the additional information and/or documentation it needs to be able to verify the claim(s) submitted by you for distribution.

7. If I am eligible for compensation, how will this be allocated?

- Participating claimants are categorised into MPCs and contractual claimants. The Steinhoff Group has made available a total settlement consideration to MPCs of SIHNV and SIHPL and contractual claimants of SIHNV of EUR612.62 million (the “SoP Gross Settlement Fund”), of which the estimated share of MPCs will be approximately EUR442 million.

- In addition, SIHPL will make available a further separate amount of ZAR 3,213,580,773 to be applied only to SIHPL MPCs on a pro rata basis (the “SIHPL MPC Gross Settlement Fund”).

- The SoP Gross Settlement Fund and the SIHPL MPC Gross Settlement Fund have been paid by SIHNV and SIHPL, respectively, to SRF in cash for distribution.

- The SoP Gross Settlement Fund and the SIHPL MPC Gross Settlement Fund will be allocated in accordance with the details set out in the Steinhoff Allocation Plan attached to the Schemes. Further details of how compensation will be allocated can also be found in the Steinhoff Allocation Plan Frequently Asked Questions.

- In addition, Steinhoff Africa Holdings Proprietary Limited, a member of the South African cluster of companies within the Steinhoff Group, has also made a contribution to the costs of the ACGs (representatives of MPCs) of EUR30 million. SIHNV has also made a contribution to the costs of SRF of EUR16.5million.

- SIHPL contractual claimants will be settled at the recovery rates and in the amounts as set out in the S155 Scheme.

- For more information on the terms for recovery from the contribution by Deloitte and the D&Os, please see part 1 above or visit www.steinhoffsettlement.com/settlements-deloitte-and-do.aspx.

8. When will I get paid my settlement consideration?

- It is expected that MPCs who do not dispute their claim determination will receive a settlement distribution as soon as reasonably practicable after the Bar Date (as defined within the Schemes) and notification of their (final) claim determination. At the same time, a settlement distribution will be made to the SIHNV contractual claimants.

- MPCs and SIHNV contractual claimants with disputed claim determinations will receive settlement distributions as soon as reasonably practicable after a binding determination in respect of their claim determination has been made.

9. I have received an Initial SIHPL Claim Valuation Notification from Computershare. What does this mean?

- The Initial SIHPL Claim Valuation Notification relates solely to the S155 Scheme and is intended to notify you of: (i) the fact that Computershare, as the Claims Administrator, has initially determined that the claim you filed for the purposes of the S155 Scheme constitutes an “MPC Relevant Claim” pursuant to the S155 Scheme Proposal and can be accepted; and (ii) the claim value of that claim insofar as it relates to SIHPL Shares (the “Initial SIHPL Claim Value”).

- If you have received an Initial SIHPL Claim Valuation Notification, it means that you are eligible to participate and/or vote at the S155 Scheme meeting.

- For the avoidance of doubt, the Initial SIHPL Claim Value ascribed to your claim has been initially calculated solely in relation to the SIHPL Shares filed in the claim and is not conclusive for the purposes of distribution. No rights can be derived from the Initial SIHPL Claim Value Notification in the context of the distribution. Prior to a distribution being made, the Claims Administrator may re-verify the claim. In respect of that process, you will be entitled to cure any deficiencies and may avail yourself of the full Dispute Committee process for distribution purposes as set out in the S155 Scheme Proposal.

- If you believe that the Initial SIHPL Claim Value Notification contains any manifest error or misapplication of the Steinhoff Allocation Plan, pursuant to the SIHPL Section 155 Proposal you must notify the Validation Committee of this by 11:59:59pm SA time on Monday 16 August 2021. The contact details of the Validation Committee are: [email protected]. If you wish to use it, template disagreement wording is available on the Steinhoff Settlement Website (www.steinhoffsettlement.com) via the “s155 Validation Process” tab.

10. I have received a Deficiency Notification from Computershare. What does this mean?

- The Deficiency Notification relates solely to the S155 Scheme and is intended to notify you of your ineligibility to participate in and vote at the S155 Scheme meeting, on the basis that one or more deficiencies have been found in respect of the claim submitted by you in the context of the S155 Scheme (i.e. only in respect of your SIHPL Shares).

- Please note that the Deficiency Notification does not mean that you are not eligible to receive a distribution from the settlement fund. For distribution purposes, you will be entitled to cure any deficiencies and may avail yourself of the full Dispute Committee process as set out in the S155 Scheme Proposal. If you are able to cure these deficiencies (and any potential further deficiencies that are notified to you by the Claims Administrator at a later stage), you may still be eligible to receive a distribution from the settlement fund. The Claims Administrator will contact you in due course with an outline of the additional information and/or documentation it needs to be able to verify the claim(s) submitted by you for distribution.

- If you believe that any deficiency(ies) identified by the Claims Administrator in the Deficiency Notification contains any manifest error or misapplication of the Steinhoff Allocation Plan, pursuant to the SIHPL Section 155 Proposal you must notify the Validation Committee of this by 11:59:59pm SA time on Monday 16 August 2021. The contact details of the Validation Committee are: [email protected]. If you wish to use it, template disagreement wording is available on the Steinhoff Settlement Website (www.steinhoffsettlement.com) via the “s155 Validation Process” tab.

11. If I am eligible for compensation under the Dutch SoP Scheme Proposal and/or S155 Scheme Proposal, how will this be allocated?

- Participating claimants are categorised into MPCs, contractual claimants and financial creditors. The Steinhoff Group will make available a total settlement consideration to MPCs of SIHNV and SIHPL and contractual claimants of SIHNV of EUR612.62 million (the “SoP Gross Settlement Fund”), of which the estimated share of MPCs will be EUR442million.

- In addition, SIHPL will make available a further separate amount of ZAR 3,213,580,773 to be applied only to SIHPL market purchase claims on a pro rata basis (the “SIHPL MPC Gross Settlement Fund”).

- The SoP Gross Settlement Fund and the SIHPL MPC Gross Settlement Fund will be paid by SIHNV and SIHPL, respectively, through SRF: 50 per cent in cash and 50 per cent in shares indirectly owned by SIHNV in the South African entity Pepkor Holdings Limited (“PPH”) at a deemed share price of ZAR15 per share, provided that SIHNV and SIHPL (as applicable) each reserve the option to settle a higher proportion of the consideration in cash.

- The SoP Gross Settlement Fund and the SIHPL MPC Gross Settlement Fund will be allocated in accordance with the details set out in the Steinhoff Allocation Plan attached to the Schemes.

- In addition, SAHPL will make a contribution to the costs of the ACGs (representatives of MPCs) of up to EUR30million, contingent on certain terms and conditions. SIHNV will also make a contribution to the costs of SRF estimated to be up to EUR16.5million.

- SIHPL contractual claimants will be settled at the recovery rates and in the amounts as set out in the S155 Scheme Proposal. By way of variation to the October Settlement Term Sheet, BVI No 1499 (Pty) Limited ("BVI") will receive PPH shares at a deemed price per share of ZAR13 (as opposed to ZAR13.5) and the lock up period applicable to BVI and Cronje claimants has been reduced.

- For more information on the terms for recovery from the contribution by Deloitte and the D&Os, please see part 1 above or visit www.steinhoffsettlement.com/settlements-deloitte-and-do.aspx.

12. When will I get paid my settlement consideration?

- It is expected that (i) SIHPL contractual claimants will receive their settlement distributions as soon as possible after the Settlement Effective Date (as defined within the Schemes) and (ii) SIHPL MPCs (or SIHNV MPCs under the Dutch SoP Scheme proposal) who do not dispute their claim determination will receive their settlement distribution as soon as reasonably practicable after the Bar Date (as defined within the Schemes) and notification of their (final) claim determination. At the same time, settlement distribution will be made to the SIHNV contractual claimants under the Dutch SoP Scheme Proposal.

- SIHPL MPCs (and SIHNV MPCs under the Dutch SoP Scheme proposal) and SIHNV contractual claimants with disputed claim determinations will receive their settlement distributions as soon as reasonably practicable after a binding determination in respect of their claim determination has been made.

Part 3 – Benefits and terms of the Steinhoff Group Settlement

1. What will settlement mean for Steinhoff’s future?

- Settlement of the outstanding litigation is essential to secure a future for the Steinhoff Group. Prior to the Steinhoff Group Settlement, Steinhoff’s liabilities exceeded its assets and it had in excess of EUR 9 billion of centrally borrowed financial debt in addition to the claims – this was an unsustainable situation and reducing its indebtedness to a more manageable level was critical to its future. However, at present, the Steinhoff Group was facing legal claims of c. EUR 10 billion and these must be addressed before any plan to deleverage can be developed and implemented.

- The Steinhoff Group Settlement will also free up Steinhoff management’s time and resources currently dedicated to the conduct of litigation and settlement negotiations, which could be re-directed towards the ongoing restructuring and improving the Steinhoff Group’s underlying businesses.

- The settlement will provide litigation claimants with certainty, compared with the cost and uncertainty of continuing with protracted, expensive and unpredictable court processes in pursuing their claims.

2. How have you arrived at the value of the various settlements and why do you believe it is fair?

- Steinhoff has formulated the settlement amounts for various claimant groups in light of the characteristics of, and risks affecting, their claims, the Steinhoff Group’s ability to continue trading and maximise the asset value available to it, and the likely outcomes for claimants if Steinhoff was unable to do so and liquidation ensued.

- In respect of ‘Market Purchase Claims’ against Steinhoff, the Steinhoff Group engaged Analysis Group to provide expert advice and to develop a methodology for calculating alleged claims against Steinhoff for the purposes of allocating settlement consideration. Steinhoff believes that this methodology is reasonable and market standard in similar securities litigation cases.

- In respect of ‘Contractual Claims’ against Steinhoff, the Steinhoff Group has calculated alleged claims based on a recommended loss methodology developed by its legal and financial advisers.

3. What are the terms of the Steinhoff Group Settlement for the financial creditors?

- The SIHNV and SIHPL financial creditors holding claims against SIHNV or SIHPL arising out of, under or in connection with contingent payment undertakings (“CPUs”) or, in the case of SIHPL’s financial creditors, the new S155 Settlement Note (as explained below) (other than creditors holding claims under the Hemisphere International Properties B.V. CPU), will not be eligible to receive any distribution as part of the settlement in respect of their claims arising out of, under or in connection with the SIHNV CPUs and the S155 Settlement Note.

- Instead, they have been asked to provide their consent for the Steinhoff Group Settlement and, in the case of SIHNV financial creditors, for their consent to extend the maturity date of the SIHNV CPUs and the underlying debt obligations by 18 months to 30 June 2023 with an option for a further 6-month extension on the approval of a lower CPU creditor voting threshold. The extension of the debt is to provide the Steinhoff Group with the breathing space to implement the settlement. SIHNV financial creditors will also be required to waive any tortious (delictual) claims they may have against the Steinhoff Group, D&O insurers and auditors.

- The SIHPL financial creditors have been asked to waive any and all claims against SIHPL arising under, out of or in connection with the SIHPL CPU in consideration for a settlement loan note against SIHPL under the S155 Scheme that will be eligible for payment over time (the “S155 Settlement Note”). SIHPL financial creditors have also been required to waive any tortious (delictual) claims they may have against the Steinhoff Group, D&O insurers and auditors. Under the S155 Settlement Note, the SIHPL financial creditors agree that (i) their rights of recourse in respect of their claims will be limited to the assets ultimately available to meet them so that the ultimate levels of recovery on their claims will depend on the value of such assets, will remain uncertain and may differ materially from the absolute amounts of their claims and (ii) such limited recourse claims will be subject to third ranking security granted by SIHPL. An update in this respect was contained in the July 2021 Settlement Term Sheet and in this regard we refer you to the 'Summary Amendments to the terms of the Steinhoff Group Settlement' available on www.steinhoffsettlement.com/case-documents.aspx.

- SIHNV financial creditors will maintain their rights under the SIHNV CPUs and be granted security over SIHNV’s shares in a subsidiary (Steinhoff Investment Holdings Limited) in respect of their post-settlement claims. Conversely, they have agreed that their rights of recourse in respect of their claims will be limited to the assets ultimately available to meet them so that the ultimate levels of recovery on their claims will depend on the value of such assets, will remain uncertain and may differ materially from the absolute amounts of their claims. Moreover, the SIHNV financial creditors will extend the maturities under the SIHNV CPUs to 30 June 2023, with the possibility of a further six months’ extension, in case of the successful implementation of the Steinhoff Group Settlement.

4. If a claimant still holds Steinhoff shares from before December 2017, do they have to give them back in exchange for the settlement consideration?

- Claimants are entitled to keep the SIHNV shares they currently own.

5. Will all shareholders that purchased shares on the open market be treated equally in the settlement?

- All shareholders that purchased Steinhoff shares resulting in eligible claims against SIHPL and/or SIHNV will be treated equally, taking into account the date on which they purchased shares and the assumed inflation of the share price on that date in accordance with the inflation methodology (as set out in the Steinhoff Allocation Plan).

6. How are individual / retail shareholders being catered for?

- The Public Investment Corporation and other asset managers that invested on behalf of pension funds are all able, and are encouraged, to participate in the settlement.

- As a key purpose of the settlement is to allow for the continued operations of the Steinhoff Group, there is also an opportunity for those individuals who are still shareholders of SIHNV to realise value on their investments.

7. Why are the SIHPL Contractual Claimants getting a higher recovery than the MPCs?

- Contractual claimants assert claims based on direct dealings with Steinhoff culminating in a contract for the acquisition of shares by exchange, subscription or purchase.

- Specifically, such claimants assert legal entitlements to rescind or cancel contracts on the alleged basis that they were entered into as a result of misrepresentations by Steinhoff’s representatives in pre-contractual negotiations and seek to claim back from Steinhoff the consideration paid for the shares; alternatively they seek to claim damages in lieu of cancellation or restitution of that consideration.

- The methodology pursuant to which the contractual claimants are compensated reflects the legal nature of these claims.

- By contrast, market purchase claimants did not deal directly or contract with Steinhoff when they acquired shares. Such claims face material legal complexity relative to contractual claims.

- As the recent South African judgment in the De Bruyn case shows, an absence of direct dealing with Steinhoff means there are higher legal hurdles for market purchase claimants in establishing that SIHPL owed them legal liability in respect of their share purchases. Such claimants may also face obstacles with respect to evidencing reliance on the alleged misrepresentations at the time that they transacted, and establishing or quantifying recoverable loss. The differentiation in recoveries at SIHPL between market purchase claimants and contractual claimants reflects these material legal uncertainties and the material litigation risk affecting the market purchase claims.

- The settlement terms propose that market purchase claimants be compensated with reference to a methodology that estimates the extent of the price “inflation” in their shares attributable to alleged misrepresentations in Steinhoff’s public disclosures at the time that they acquired the relevant shares from third parties in the market. This type of methodology is a recognised basis of assessing the quantum of claims of class action securities claimants and allocating settlement consideration amongst them, and Steinhoff considers it the appropriate approach to use here.

8. Why is the pay-out so low relative to the claims?

- It has always been Steinhoff’s intention to provide some degree of value for shareholders who held shares at 5 December 2017 and who suffered losses. Any settlement needs to be considered against the background of the financial position of the Steinhoff Group and its very significant levels of financial indebtedness and the effect of adverse currency movements, as well as certain legal uncertainties affecting the claims. Steinhoff believes the terms are fair and realistic in the circumstances.

- A global settlement of litigation claims was contemplated when the Steinhoff Group’s EUR 9.2 billion financings were restructured and extended by agreement of its financial creditors in August 2019.

- The terms of the settlement represent value for claimants materially in excess of the permission granted by financial creditors for such a settlement at that time and will therefore require fresh consent from financial creditors, who will also be required to make certain further concessions, including the extension to the maturity of their loans to the Group by 18 months (with an option to extend for a further 6 months on further lender consent). For more information on the lender consent process, please refer to part 1, question 1.

9. Couldn’t you sell down more of PPH and increase the pay-outs?

- PPH remains a key strategic asset of the Steinhoff Group, and it is important for the preservation of value for all stakeholders that Steinhoff retains a substantial shareholding in PPH.

- The total available for settlement has to take into account the claims of all stakeholders, including the financial creditors (whose support is critical for the success of any implementation).

10. How much debt does the Steinhoff Group have and what is the current net asset value?

- The Steinhoff Group had total borrowings in excess of EUR 11.2 billion as at 30 September 2021, made up of EUR 1.4 billion at OpCo level and EUR 9.8 billion within Corporate and Treasury services (which continue to accrue interest).

- Please see the Annual Report for the year ended 30 September 2021, which was published on 15 December 2021, and which is available to download at the following web-address: https://www.steinhoffinternational.com/annual-reports.php.

Steinhoff Allocation Plan Frequently Asked Questions

In this section, you will find Frequently Asked Questions about the allocation plan that is set out at Schedule 3 (Steinhoff Allocation Plan) to the Dutch SoP Scheme and as referred to in the S155 Scheme (the “Steinhoff Allocation Plan”). Capitalised terms used but not defined in this Frequently Asked Questions section have the meaning given to them in the Steinhoff Allocation Plan.

These Frequently Asked Questions have been published to assist claimants with SIHNV’s and SIHPL’s global settlement of claims (the “Steinhoff Group Settlement”) and are only non-binding guidance for MPC Claimants and should be read in conjunction with the SIHNV’s composition plan as submitted in the Dutch SoP (“Dutch SoP Scheme”) and SIHPL’s plan under the South African S155 (“S155 Scheme”) (together the “Schemes”) (including the Steinhoff Allocation Plan), as applicable. If there is an inconsistency between these Frequently Asked Questions and the Schemes (including the Steinhoff Allocation Plan), the provisions of the Schemes (including the Steinhoff Allocation Plan) will prevail.

Please note that the answers do not constitute legal advice. Please consider the terms of the Schemes carefully to make sure you understand your position. The Schemes are complex documents and claimants should obtain independent legal, financial and tax advice in relation to the Schemes and the claim administration Only the Schemes (including the Schedules and Annexes thereto) contain the terms and conditions on the basis of which any claimant may or may not hold any entitlement to any distribution. These Frequently Asked Questions are not intended to reflect all of such terms and conditions and do not in any way alter, modify, supplement or otherwise grant such right or obligation to any claimant, any member of the Steinhoff Group or the SRF (as defined below). This is a document that in itself does not have any legal power or authority. None of the Steinhoff entities nor their advisers are providing any advice to the claimants or any other party.

A. What is the Steinhoff Allocation Plan and how does it apply to me?

1. What is the Steinhoff Allocation Plan?

- the value of each MPC Claimant’s claim against Steinhoff will be calculated; and

- the amount of money each MPC Claimant is entitled to receive in settlement of their respective claim will be allocated.

The exact share of the SoP Settlement Fund to which you may be entitled cannot be calculated yet as it depends on, among other things, the total value of all relevant claims that are admitted against SIHNV and/or SIHPL and reviewed by the Claims Administrator. At present, it is not known how many MPC Claimants have eligible claims against SIHNV and/or SIHPL and so it is not possible to predict with certainty the total value of all relevant claims that are to be admitted and reviewed.

Please refer to question 9 for an illustration of how an MPC Claimant’s share of the SoP Settlement Fund will be calculated in practice.

In addition, if you purchased shares before the Scheme of Arrangement, and have a positive SIHPL MPC Claim Value, you may be entitled to receive recovery from the SIHPL MPC Settlement Fund as described in the Steinhoff Allocation Plan. Such recovery will be in addition to the recovery from the SoP Settlement Fund.

Please refer to questions 10 and 11 for more information on the SIHPL MPC Settlement Fund and for an illustration of how an MPC Claimant’s share of this will be calculated in practice.

2. What are the “Steinhoff Shares”?

- common stock shares in Steinhoff International Holdings N.V. (“SIHNV”) with ISIN NL0011375019 (“SIHNV Shares”); and

- ordinary shares in Steinhoff International Proprietary Limited (“SIHPL”) with ISIN ZAE000016176 (“SIHPL Shares”).

3. What is an “MPC Claimant” and how do I know whether I am one?

In summary, you may be an MPC Claimant if you:

- acquired SIHPL Shares listed on the Johannesburg Stock Exchange (“JSE”) between open of business on 2 March 2009 and close of business on 6 December 2015; and/or

- acquired SIHNV Shares listed on the JSE or the Frankfurt Stock Exchange (“FSE”) between close of business on 6 December 2015 and close of business on 5 December 2017; and/or

- were not the original purchaser of the relevant shares, but had these transferred to you, for example because of a gift or inheritance (i.e. a “transfer in”); and

- in each case, continued to hold at least some of those shares (or, in the case of SIHPL Shares, some of the SIHNV Shares received in exchange for them) at close of business on 5 December 2017.

4. I acquired SIHPL Shares listed on the Johannesburg Stock Exchange before open of business of 2 March 2009. Will I have a claim?

This is referred to as a “Holder Claim” in the Steinhoff Allocation Plan and will be valued at EUR 0.01 per share still held at close of business on 5 December 2017.

5. Who is entitled to compensation in accordance with the Steinhoff Allocation Plan?

- you are an MPC Claimant;

- you continued to hold Steinhoff Shares at close of business on 5 December 2017;

- your claim has a positive value (as initially determined by the Claims Administrator);

- you filed your claim with sufficient evidence and in a valid and timely manner; and

- your claim was accepted by the SRF as an MPC Relevant Claim (please refer to question 13 of the Frequently Asked Questions for further details on the SRF).

You may also be entitled to compensation if you have a Holder Claim, i.e.:

- you acquired SIHPL Shares listed on the JSE prior to open of business of 2 March 2009 (which were subsequently converted to SIHNV Shares); and

- you held at least some of those SIHNV Shares until close of business on 5 December 2017.

6. What is a “SIHPL MPC Claimant” and how do I know whether I am one?

In summary, you may be a SIHPL MPC Claimant if you:

- acquired SIHPL Shares listed on the JSE between open of business on 2 March 2009 and close of business on 6 December 2015 (which were subsequently converted to SIHNV Shares); and/or

- acquired SIHPL Shares listed on the JSE prior to open of business of 2 March 2009 (which were subsequently converted to SIHNV Shares); and/or

- were not the original purchaser of the relevant shares, but had these transferred to you, for example because of a gift or inheritance; and

If you are a SIHPL MPC Claimant, you may be entitled to additional compensation under the Steinhoff Allocation Plan, provided that:

- you continued to hold Steinhoff Shares at close of business on 5 December 2017;

- your claim has a positive value (as initially determined by the Claims Administrator);

- you filed your claim with sufficient evidence and in a valid and timely manner; and

- your claim was accepted by the SRF as a SIHPL MPC Relevant Claim (please refer to question 13 of the Frequently Asked Questions for further details on the SRF).

7. What is “Estimated Inflation”?

MPC Claimants’ claims will be calculated by reference to the Estimated Inflation on the days they purchased or sold shares (or, in the case of a transfer in or a transfer out, by reference to the Estimated Inflation on the date that the Steinhoff Shares were originally purchased for consideration (the “Original Purchase”)). An overview of the Estimated Inflation per day is attached to the Steinhoff Allocation Plan (see Annex 2 (Daily Average Share Price Inflation)).

8. What is the relevance of the Schemes, and how can I find out which applies to me?

- proceedings (referred to as the “South African S155”) under section 155 of the South African Companies Act 71 of 2008, which has been used to give effect to the settlement of claims against SIHPL; and

- Dutch suspension of payment (referred to as the “Dutch SoP”) proceedings, which has been used to give effect to the settlement of claims against SIHNV.

The Dutch SoP Scheme and the S155 Scheme are the documents which set out the terms of the Steinhoff Group Settlement that were approved by the courts in the relevant proceedings.

If you have a claim against SIHNV (i.e. because you purchased or acquired SIHNV Shares or had these transferred to you in the period from 7 December 2015 and continued to hold these until close of business on 5 December 2017), the Dutch SoP Scheme will apply to you.

If you have a claim against SIHPL (i.e. because you purchased SIHPL Shares (or had these transferred to you) in the period prior to 6 December 2015 and continued to hold SIHNV Shares received in exchange for such SIHPL Shares until close of business on 5 December 2017), the S155 Scheme will apply to you.

If you have claims against SIHNV and SIHPL, both the Dutch SoP Scheme and the S155 Scheme will apply to you with respect to the relevant element of your claim. Please refer to the Claim Form available at www.steinhoffsettlement.com for further information on how to submit your claim in the respective proceedings.

9. How will the settlement payment be allocated?

The exact proportion to which you may be entitled cannot be calculated yet. This is because the settlement funds made available by Steinhoff are fixed at EUR 612,620,000 (minus certain costs and expenses) (referred to as the SoP Settlement Fund), and it must be shared between all MPC Claimants and the SIHNV contractual claimants. Your settlement payment is, therefore, contingent on the total value of claims that are accepted.

The total aggregated Claim Value will be used to determine your Steinhoff MPC Settlement Payment Share.

If you are a SIHPL MPC Claimant, i.e. (part of) your claim arises from purchases of SIHPL Shares, you may also be entitled to a payment from the SIHPL MPC Settlement Fund (the “SIHPL Steinhoff MPC Settlement Payment Share”). We explain this further in questions 10 and 11.

The following are illustrations of how the Steinhoff MPC Settlement Payment Share will be calculated in practice:

Example A

- If the actual value of accepted Claims is EUR 6,300m, and reservations are made in respect of a further asserted or estimated value of EUR 700m in Claims which are disputed, an MPC Claimant with a determined Claim Value of EUR 1.5m will be entitled to payment as follows:

- This would represent a recovery of approximately 8.75% on the Claim Value of the SIHNV MPC Claimant.

Example B

- If the actual value of accepted Claims is EUR 5,400m, and reservations are made in respect of a further asserted or estimated value of EUR 600m in Claims which are disputed, a SIHNV MPC Claimant with a determined Claim Value of EUR 1.5m will be entitled to payment as follows:

- This would represent a recovery of approximately 10.2% on the Claim Value of the SIHNV MPC Claimant.

For further information on the calculation of the Steinhoff MPC Settlement Payment Share, please refer to Part V (Distribution of the SoP Settlement Fund) of the Steinhoff Allocation Plan.

10. When am I entitled to a payment from the SIHPL MPC Settlement Fund?

11. How will the SIHPL MPC Settlement Fund be allocated?

The exact proportion to which you may be entitled cannot be calculated yet. This is because the settlement funds made available by Steinhoff are fixed at ZAR 3,214m (minus certain costs and expenses) (referred to as the SIHPL MPC Settlement Fund), and it must be shared between all SIHPL MPC Claimants. Your settlement payment is therefore contingent on the total value of SIHPL MPC Relevant Claims that are accepted.

The value of your SIHPL MPC Relevant Claims will be used to determine your SIHPL Steinhoff MPC Settlement Payment Share. The allocation calculation and logic is identical to that described in question 9 above, except that only SIHPL MPC Relevant Claims are entitled to payment and included in the calculation.

Example

- If the actual value of accepted SIHPL MPC Relevant Claims is ZAR 25,000m, and reservations are made in respect of a further asserted or estimated value of ZAR 8,500m in Claims which are disputed, a SIHPL MPC Claimant with a determined SIHPL MPC Claim Value of ZAR 85m will be entitled to payment as follows:

B. Who are the key people and organisations involved?

13. What is the SRF and what will be its role?

14. Will the SRF be independent of Steinhoff?

15. Who is the Claims Administrator and what is their role?

The SRF has engaged a Claims Administrator (Computershare) to assist with the claims administration and to validate claims. The Claims Administrator is an entity that is independent of SIHNV, SIHPL and all other Steinhoff Group Companies. The role of the Claims Administrator is to assist the SRF with the implementation of the Steinhoff Group Settlement, including by:

- reviewing claims submitted by MPC Claimants;

- calculating the Claim Values for final determination by SRF; and

- assisting the SRF with the distribution of compensation to eligible MPC Claimants.

If there is anything about any of the documents or supporting evidence that you are unsure about, please give the Claims Administrator a call on:

Toll-free US number: +1 866-559-7591UIFN toll-free international number: +49 (0) 800-2667-8831

Toll-free South Africa number: +27 (0) 860 024 737

Lines are open weekdays between 8am and 4:30pm SAST.

There are trained personnel on the other side who will be able to assist you in filling out the forms correctly. In any event, we urge you to consider seeking independent legal advice prior to submitting your claim.

If the Claims Administrator needs any more details from you during the process, for example if your information appears to be incorrect or any supporting documentation is missing, they will let you know by email (at the address you have provided in your submitted Claim Form). Please respond to these requests in a timely manner, and in any event within 30 Business Days of the request. If you fail to do so, you risk the rejection of your claim.

16. Who will contact me in respect of acceptance or rejection of my claim?

If you disagree with the Claim Determination, you should let the SRF know as soon as possible, and in any event within 30 Business Days after the Claims Administrator notified you of the Claim Determination. For an explanation of the disputes process, please refer to the Dispute Committee Rules that can be found at www.steinhoffsettlement.com.

17. Who can I contact if I have any questions?

If you have any questions about the Steinhoff Allocation Plan or about the Steinhoff Group Settlement more generally, please contact the Claims Administrator on:

Toll-free US number: +1 866-559-7591UIFN toll-free international number: +49 (0) 800-2667-8831

Toll-free South Africa number: +27 (0) 860 024 737

Lines are open weekdays between 8am and 4:30pm SAST.

C. How should I make a claim?

18. What do I have to do to submit my claim for review by the Claims Administrator?

If you have signed up with a Claimant Representative, please get in touch with your contact person at that Claimant Representative.

Otherwise, please fill in the online Claim Form available at www.steinhoffsettlement.com and submit this, along with the relevant supporting evidence listed in the Claim Form, via the online portal by the Bar Date. Further details in this regard are contained in the Schemes and the schedules thereto (especially Schedule 2 to the SRF and Claims Administration Conditions (Required Claim Information). These SRF and Claims Administration Conditions are available at www.steinhoffsettlement.com.

We understand that completing the Claim Form and gathering the supporting evidence may be time consuming. However, the purpose of the Claim Form and supporting evidence is to make sure that the Claims Administrator has all the information it needs to accurately value your claim. If your claim is submitted without the required documentation, you risk the rejection of your claim. If your claim is not submitted in a timely manner, your claim will be rejected.

We understand that completing the Claim Form and gathering the supporting evidence may be time consuming. However, the purpose of the Claim Form and supporting evidence is to make sure that the Claims Administrator has all the information it needs to accurately value your claim. If your claim is submitted without the required documentation, you risk the rejection of your claim. If your claim is not submitted in a timely manner, your claim will be rejected.

19. What is the “Claim Form” and where can I find it?

Toll-free US number: +1 866-559-7591

UIFN toll-free international number: +49 (0) 800-2667-8831

Toll-free South Africa number: +27 (0) 860 024 737

Lines are open weekdays between 8am and 4:30pm SAST.

20. Is there a deadline by which I must submit my claim?

21. What will happen if I do not file a Claim Form?

22. If I do not file a Claim Form, will I be able to pursue SIHNV or SIHPL in court for an MPC Relevant Claim?

This means that, if you choose not to file a Claim Form (or you fail to file a valid Claim Form by the Bar Date):

- you will NOT be entitled to receive any compensation as part of the Steinhoff Group Settlement; and

- you will NOT be entitled to claim any compensation in (legal) proceedings for an MPC Relevant Claim against SIHNV or SIHPL after the Settlement Effective Date.

23. Why am I being asked to provide ID?

- For natural persons (i.e. individuals): a photocopy of their identity book/card (applicable to South African MPC Claimants only) or passport;

- For corporate entities: photocopies of the registration/incorporation documents; and

- For trusts: photocopies of the trust deed and the letters of authority of trustees.

This is necessary in order to allow the Claims Administrator to carry out its verification checks.

If you fail to provide the necessary identity documents when you file your Claim Form, the Claims Administrator will contact you to request them – this may cause a delay to the processing of your claims.

Your privacy is important to us. Please contact the Claims Administrator if you have any questions about how your personal data will be processed.

24. What is the significance of the 6 December 2015, 5 December 2017 and 6 December 2017 dates?

Close of business on 6 December 2015 was when you could last purchase or acquire shares in SIHPL, and therefore have a claim against SIHPL. At open of business on 7 December 2015 the shares in SIHPL were exchanged for shares in SIHNV through the Scheme of Arrangement. Any shares purchased or acquired after open of business on 7 December 2015 would result in claims against SIHNV.

5 December 2017 and 6 December 2017 are the dates on which Steinhoff made the following “curative disclosures”, in the form of press releases, in which it identified the presence of suspected accounting irregularities and provided estimates of the potential overstatement of the value of its assets:

- after the market closed on 5 December 2017, SIHNV disclosed that it had discovered accounting irregularities and that CEO Markus Jooste had tendered his resignation with immediate effect; and

- after the market closed on 6 December 2017, SIHNV announced that it had identified issues with the “validity and recoverability” of “circa €6bn” in assets.

In addition, Steinhoff made a “partial” curative disclosure of the alleged accounting irregularities on 4 December 2017 with an announcement that the forthcoming annual financial statements would be disclosed in unaudited form.

These three dates are used by SIHNV’s and SIHPL’s economic expert, Analysis Group, to estimate the alleged inflation (the “Estimated Inflation”) in the Steinhoff Shares during the Relevant Period (i.e. the period commencing on 2 March 2009 through to close of business on 6 December 2017), which is in turn used to calculate the Claim Value of each MPC Claimant’s claim.

It is important to note that Steinhoff denies any wrongdoing.

25. I held Steinhoff Shares in multiple trading accounts. Am I permitted to submit a separate Claim Form for each trading account?

If it becomes apparent to the Claims Administrator that you (or your representative) have filed two or more Claim Forms in respect of different accounts held by you, the Claims Administrator will be in touch with you (or your representative) to notify you that the claims have not been aggregated and that this needs to be rectified. In such cases, if you fail to aggregate the claims within the time specified by the Claims Administrator in the notice, your claims may be rejected in whole or in part.

26. I held SIHPL Shares and SIHNV Shares. Do I need to submit separate Claim Forms?

27. What is a duplicate claim and how will duplicate claims be dealt with?

D. How will my claim be calculated?

Please note that these examples are illustrative only and do not give any guarantee as to the total amount that you may be entitled in respect of your MPC Relevant Claims. No rights can be derived from these examples. The determination of the Claim Value of your MPC Relevant Claims will, among other things, depend on the documentary evidence provided with the Claim Form. Further examples of how an MPC Claimant’s Claim Value is calculated can be found at Annex 3 (Sample Calculations) of the Steinhoff Allocation Plan.

28. What is the difference between my MPC Claim Value and my SIHPL MPC Claim Value?

Your SIHPL MPC Claim Value is the value of your MPC Relevant Claim against SIHPL. Assuming you are a SIHPL MPC Claimant (i.e. because you, among other things, purchased some or all of your Steinhoff Shares before the Scheme of Arrangement) and you have a positive SIHPL MPC Claim Value, you may be entitled to receive recovery from the SIHPL MPC Settlement Fund as described in the Steinhoff Allocation Plan (see question 11 above). Such recovery will be in addition to the recovery from the SoP Settlement Fund.

29. If I have an MPC Relevant Claim, will I receive a payment from the SIHPL MPC Settlement Fund?

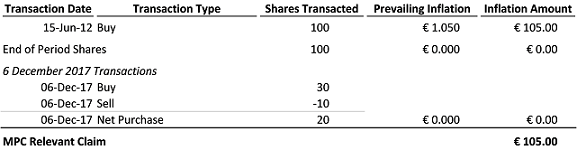

30. I purchased Steinhoff Shares during the Relevant Period and held these until close of business 5 December 2017. I did not sell any Steinhoff Shares during the Relevant Period. Do I have an MPC Relevant Claim?

Based on these facts, you should have a positive MPC Relevant Claim and you may therefore be eligible for a Steinhoff MPC Settlement Payment Share. This is because you have not sold or transferred out any Steinhoff Shares and so the Estimated Inflation for the Steinhoff Shares you purchased has not been offset by any Estimated Inflation generated by a sale.

The following example shows how this would be calculated in practice:

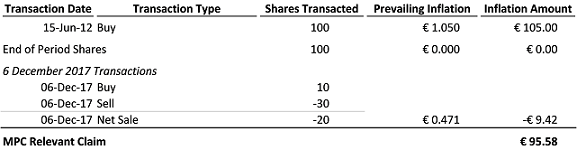

31. I purchased Steinhoff Shares during the Relevant Period and held some of these until close of business 5 December 2017. I also sold Steinhoff Shares during the Relevant Period. Do I have an MPC Relevant Claim?